TradeLingo Ai Academy

TradeLingo Ai Academy review: Great for mastering forex terminology but limited on advanced strategies. Here's an honest take after testing.

Read review

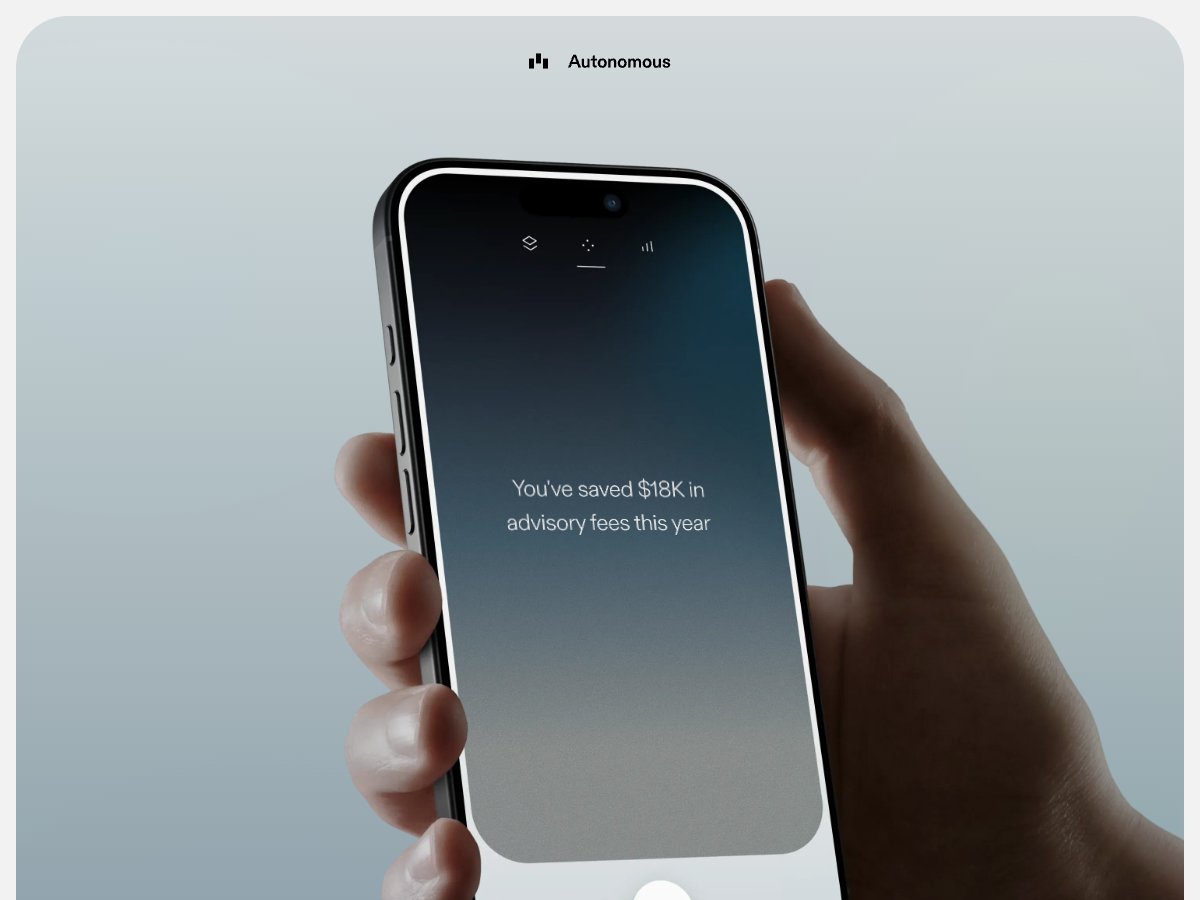

Autonomous review: Great for personalized, fee-free financial guidance but limited long-term track record. Here's my honest take after testing.

Autonomous review: Great for personalized, fee-free financial guidance but limited long-term track record. Here's my honest take after testing.

The core platform is free, offering great value. Paid features add customization but are optional based on your needs.

Yes, the main platform with tailored portfolios and guidance is free; additional features like Autonomous Index cost extra.

Autonomous offers more personalized, real-time advice and zero advisory fees, whereas Betterment is more automated and less adaptive.

Since the core service is free, refunds aren’t typical. Paid features may have specific policies—check with Autonomous.

Autonomous employs standard security measures, but always exercise caution with sensitive information online.

Yes, it supports cross-account coordination including 401(k), taxable accounts, and debt management.

Continue with tools in the same category, including screenshots and published Automateed reviews.

TradeLingo Ai Academy review: Great for mastering forex terminology but limited on advanced strategies. Here's an honest take after testing.

Read review

Creo by ZenStatement offers a versatile AI writing assistant with an affordable price, but it lacks advanced marketing features. Here's my honest...

Read review

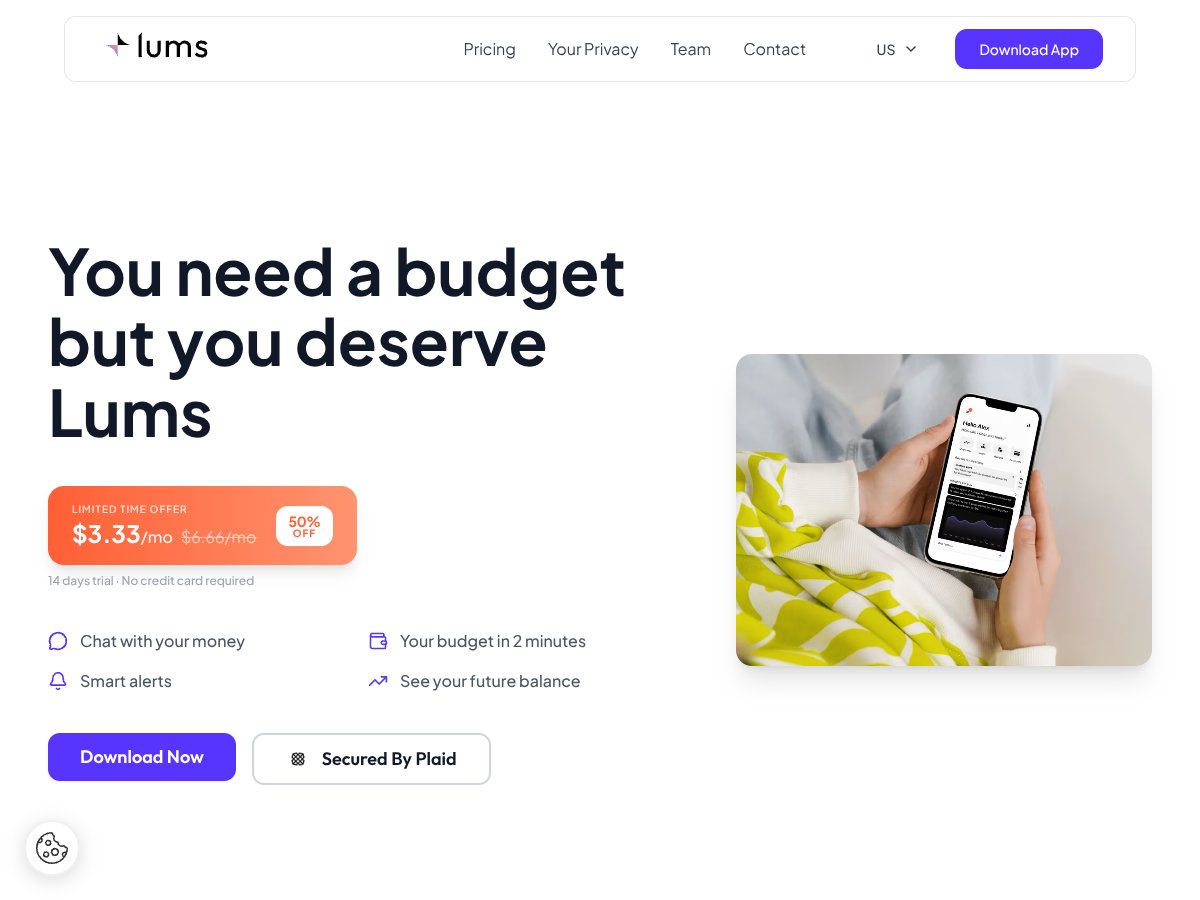

Lums review: Great for automated budgeting and forecasting but lacks user reviews and pricing info. Here's my honest assessment after testing.

Read review

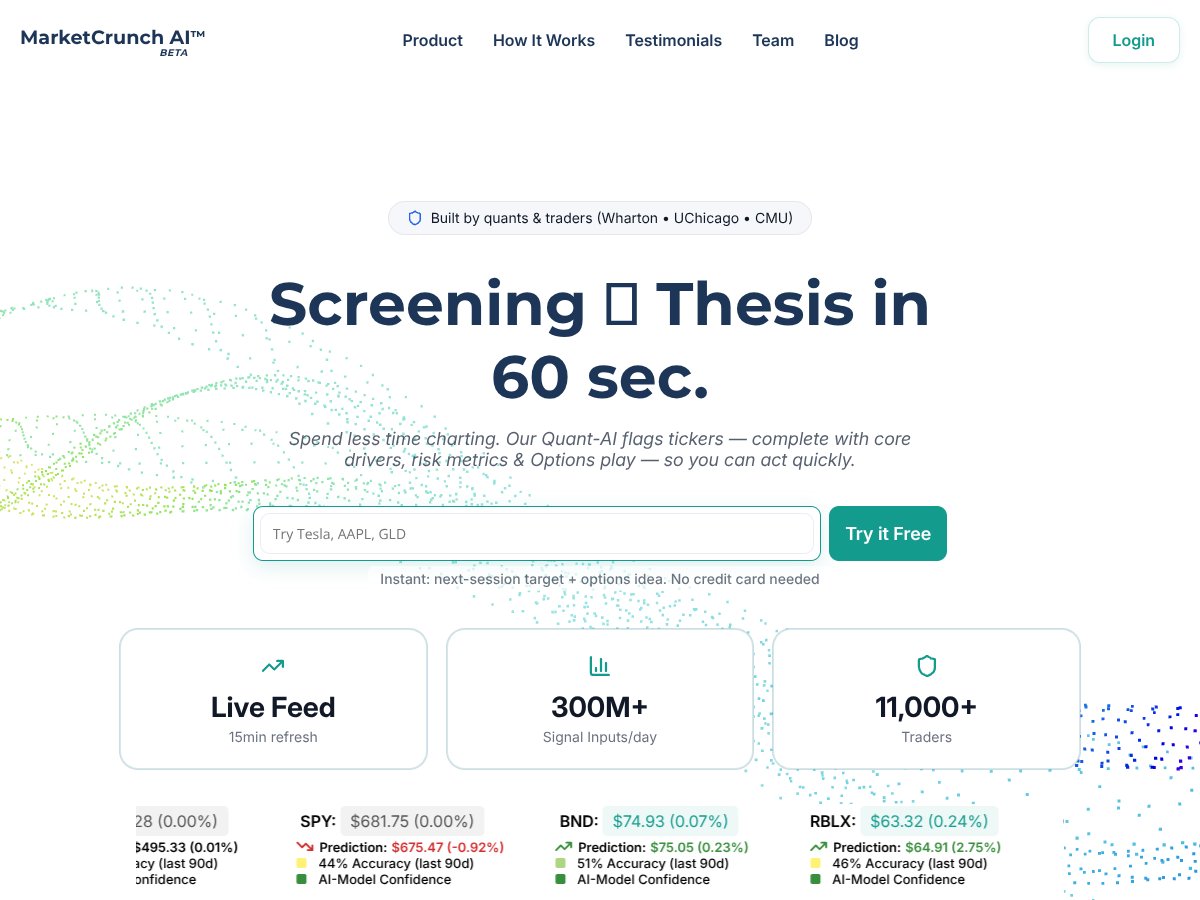

MarketCrunch AI offers explainable forecasts and real-time sentiment, but pricing details are scarce. Here's an honest review after testing it...

Read reviewAs featured on

Add this badge to your site